carried interest tax uk

While the future of carried interest and long-term capital gain tax rates may remain in flux we do have clarity on required holding periods. 9 Reporting obligations in relation to carried interest.

This Infographic Shows Just How Much Corporation Tax Amazon Starbucks And Google Have Avoided Paying And How That Money Could Be U Infographic Corporate Tax

A UK private company limited by guarantee.

. We responded to the review and produced a summary document on carried interest which includes international comparisons. And that planning. In fact the only other asset which is taxed at 28 is residential property.

Were positioned to help you assess and comply with the new carried interest tax rules while seamlessly integrating with your funds operations. The carried interest rules impose a minimum 28 per cent tax on carried interest distributions to UK resident fund managers subject to potential reduction for those who are non-domiciliaries. Although it is true that carried interest gains are taxed at 28 this is a special higher rate than would be paid on other gains on share sales taxed at a maximum of 20.

Historically carried interest returns have been taxed as capital gains arising on the disposal of a funds underlying investment a treatment preserved by the DIMF rules. Printable version Send by email PDF version. We are aware of an increase in the number of enquiries into the tax treatment of carried interests HMRC are raising at a House level as well as at an individual level.

Availability of business asset disposal relief and investors relief. This can be as much as 20 at a higher rate or 28 on real estate assets. The new carry rules have effect in relation to carried interest arising on or after 8 July.

Carried interest will be partly IBCI if the. In July 2020 the Office of Tax Simplification published a review of capital gains tax. This applies to fund managers who provide services in order to share in the funds profits also known as a carried interest or incentive allocation.

In the event that a double tax charge arises the individual will be allowed an offsetting credit in order to avoid double taxation ITA 2007 s 809EZG and TCGA 1992 s 103KE. The Carried Interest tax regimes replace any CGT charge which would have already arisen under pre-existing rules but does not replace any pre-existing income tax charge. This measure will make the tax system fairer by ensuring that individuals to whom a gain arises in the form of carried interest are taxed on their true economic gain.

Some view this tax treatment as unfair because the general partner receives carried interest as compensation for its investment management services. The top rate applicable to LTCG currently 20 is substantially lower than the top ordinary rate currently 37 and is therefore a material consideration for managers of investment partnerships. Those rules apply to carried interest arising on or after 8 July 2015 but also contained transitional rules.

Avoidance of double taxation 1 This section applies where a capital gains tax is charged on an individual by virtue of section 103KA in respect of any carried interest and b at any time tax whether income tax or another tax charged on the individual in relation to that carried interest has been paid by him or her and. Others argue that it is consistent with the tax treatment of other entrepreneurial income. Carried interest is wholly IBCI if the relevant fund holds its assets for an average of 3 years or less.

HMRC Enquiries into the Tax Treatment of Carried Interest. Additionally in April 2016 the UK government introduced legislation the income-based carried interest rules to restrict the capital gains tax. Under the current system any carried interest earned by a private equity firm from an asset held more than 40 months is taxed as capital gains.

8 Capital gains tax analysis. Our previous blog article on the new rules for the taxation of carried interest looked at their general impact on investment managers including the introduction of the concept of income-based carried interest IBCI and the rule that carried interest that is not IBCI is to be treated as giving rise to UK situs capital gains irrespective of the situs of the underlying assets. Private equity executives receiving carried interest could be in for a significant tax hike after the UK announced an investigation into the countrys capital gains tax system.

Carried interest as a notional payment. However the rate of CGT applicable to carried interest remains at 28 whereas a rate of 20 applies to most other types of capital gain. These enquiries are typically aimed at several investment management.

Unleashing the value of data in a fragmented world. Income Based Carried Interest IBCI which is subject to income tax and NIC and carried interest which is not IBCI which is subject to capital gains tax CGT. The digital economy dilemma.

Carried interest income flowing to the general partner of a private investment fund often is treated as capital gains for the purposes of taxation. Under the current rules carried interestan individual fund managers enhanced share of profits realized from investmentsis taxed as capital gains at 28 while income is taxed at a rate of at least. Carried interest has increasingly come within HM Revenue Customs focus due to the potential risk of ordinary management fees being disguised as carried interest to avoid income tax.

PAYE and NICs indemnity. Published 22 November 2017. We also published a comment piece following the OTS interim report and the New Horizons Report showcasing how the industry contributes to the UK economy and.

Carried interest now falls into one of two categories. Some view this tax preference as an unfair market-distorting loophole. 10 Capital gains tax analysis before 8 July 2015.

7 rows Under the IBCI Rules carried interest which is income-based carried interest will be taxed. Withholding employee Class 1 NICs. Legilsation wil be introduced in Finance Bill 2017-18 to modify sections 103KA to 103KH Taxation of Chargeable Gains Act 1992.

However carried interest is often treated as long-term capital gains for tax purposes subject to a top tax rate of 238 20 on net capital gains plus the 38 net investment income tax. Instead they charge their investors a management fee of 2 and keep 20 of future profits that their investments generate which is known as carried interest. Over 2015 and 2016 new rules relevant to carried interest were introduced that were designed both to reduce the scope for avoidance and to restrict the beneficial tax treatment.

Get emails about this page.

Our Approach To Tax The Heineken Company

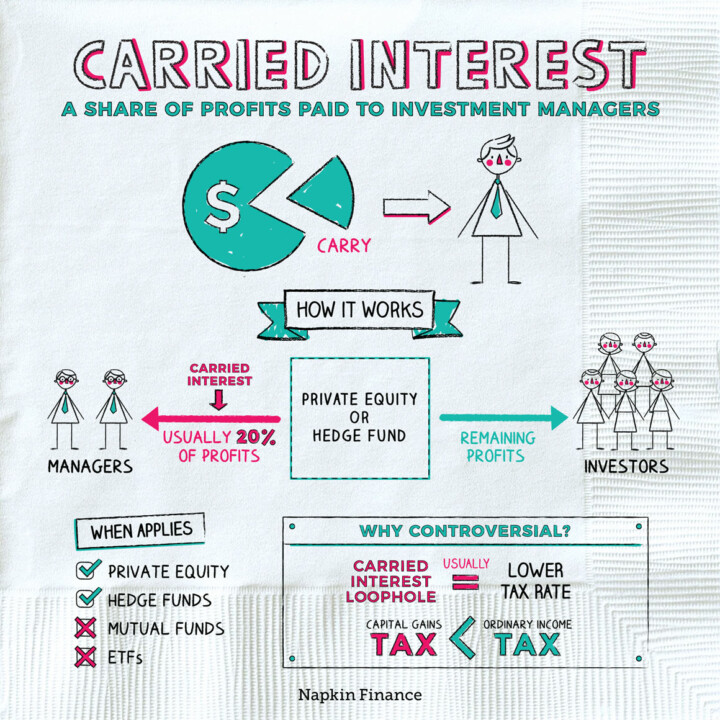

How Does Carried Interest Work Napkin Finance

Carried Interest In Private Equity Calculations Top Examples Accounting

What Tax Do I Pay On Savings And Dividend Income Low Incomes Tax Reform Group

Internal Auditors Must Consider Different Aspects Of A Business Business Performance Success Business Accounting And Finance

Building Contractor Appointment Letter How To Create A Building Contractor Appointment Letter Download This Building C Lettering Letter Templates Templates

Singaporeans Still Top Investor For Uk Property Http Overseascondo Sg Properties Royal Wharf London London Buying Property Black Brick

Why Buy In Dubai Infographic Uaedxb Dubai World Dubai Infographic

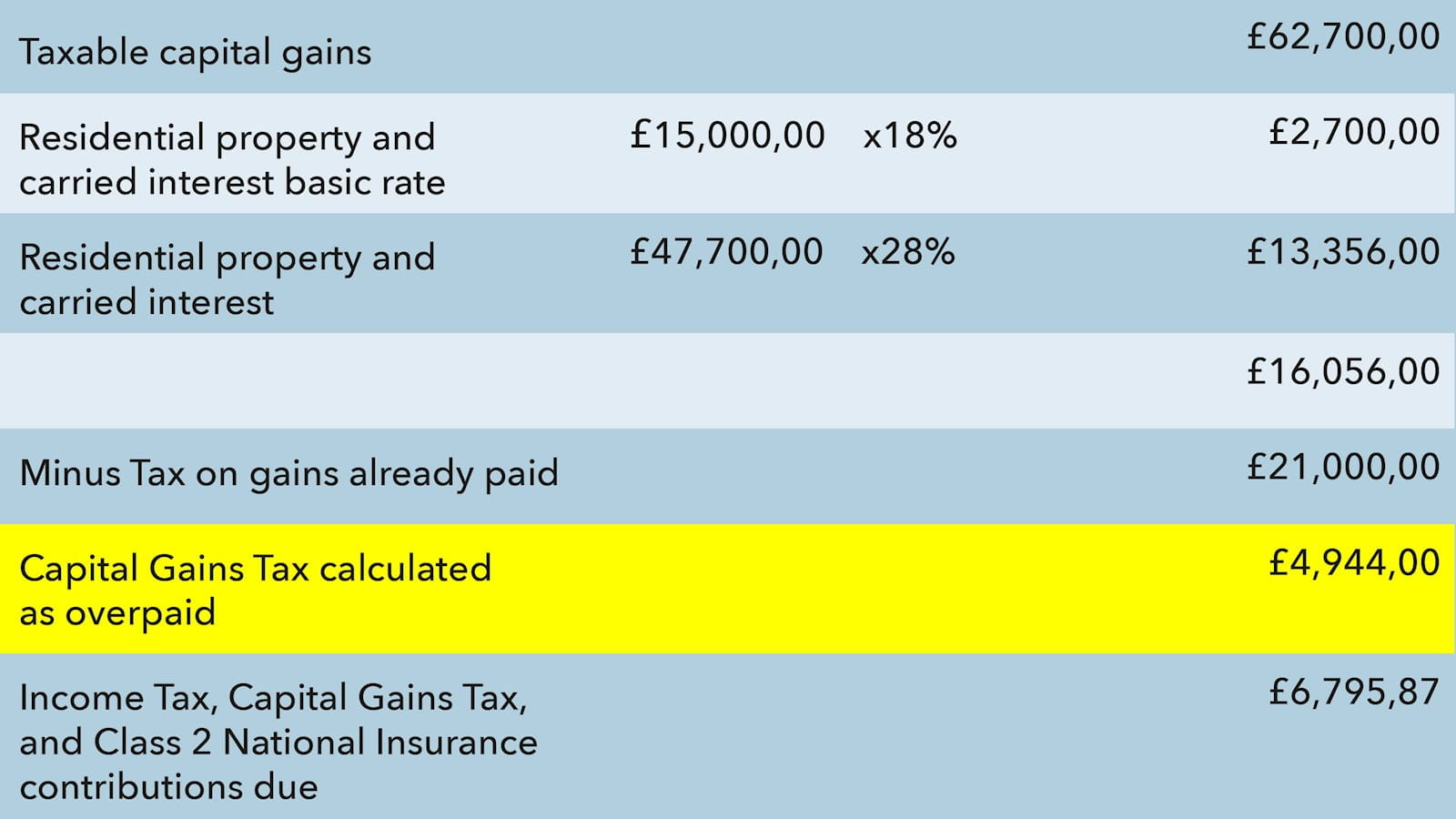

Offsetting Overpaid Cgt Against Income Tax Icaew

Taxes On Money Transferred From Overseas In The Uk Dns Accountants Money Transfer Paying Taxes Blog Taxes

Carried Interest In Venture Capital Angellist Venture

Basic Principles Of Investment Investing Lost Money Wealth Creation

Private Equity The Taxation Of Fund Managers Saffery Champness

How Can We Afford The Freedom Dividend Dividend The Freedom Financial

Why Slowly Nudging Up Interest Rates Makes Sense Investment Property Mortgage Rates Investing

How To Tax Capital Without Hurting Investment The Economist

Carried Interest Plans Can Benefit Both The Fund Management Industry And Investors Intertrust Group

Taking Goods Temporarily Out Of The Uk How To Apply Understanding United Kingdom

Einstein Tuition Private Home Tuition Singapore Private Tutors Tutor Paying Taxes